Many Irish families want to help their children and grandchildren achieve important financial milestones, whether that’s buying a first home, paying for further education, purchasing a car, or building financial security for the future. At the same time, rising property values and increasing wealth mean more families are becoming conscious of potential inheritance tax liabilities.

One often-overlooked strategy is to combine a regular savings plan with Ireland’s Small Gift Exemption. Used consistently over time, this approach can help families transfer wealth in a structured, tax-efficient manner while providing meaningful financial support to the next generation.

What Is the Small Gift Exemption?

The Small Gift Exemption allows any individual to gift up to €3,000 per year to another person without triggering Capital Acquisitions Tax (CAT). Importantly, these gifts do not reduce the recipient’s future inheritance tax threshold.

While €3,000 may not seem like a significant amount in isolation, the cumulative impact can be substantial when used year after year. Unlike some tax reliefs, any unused annual exemption cannot be carried forward. If it is not used within the calendar year, it is lost permanently.

As of 2026, children can generally inherit up to €400,000 from their parents before CAT applies. Any amount above this threshold is currently taxed at 33%. With property prices and asset values continuing to increase across Ireland, more families are finding themselves exposed to potential inheritance tax liabilities, making early planning increasingly important.

How Families Can Maximise the Benefit

One of the greatest advantages of the Small Gift Exemption is that it applies to each individual giver and recipient. For example, a mother can gift €3,000 to her child in a calendar year, while the father can also gift €3,000 to the same child. Together, parents can transfer €6,000 annually to each child completely free from CAT implications.

The benefits can increase significantly when grandparents are included in the planning process. Each grandparent can also gift up to €3,000 per grandchild every year.

For larger families, these annual tax-free gifts can quickly add up. A couple with three children could transfer €18,000 every year without triggering CAT. Over a decade, that could amount to €180,000 transferred tax-efficiently to the next generation.

This approach can help build funds for future education costs, home deposits, business ventures, or other important life events, while gradually reducing the value of an estate that may otherwise be subject to inheritance tax in the future.

Combining the Exemption with a Savings Plan

The Small Gift Exemption can be even more effective when combined with a regular savings strategy.

Instead of waiting for a large inheritance or one-off gift, many families choose to save regularly. They gradually build funds that can later be transferred using the annual exemption.

This creates a disciplined approach to both saving and transferring wealth.

For example, a parent could gift €3,000 to a child every year for 10 years. This could result in €30,000 being transferred without any CAT implications, assuming no investment growth.

If the funds are saved or invested in a suitable long-term arrangement, the value may be higher. However, investment returns are not guaranteed.

Such a fund could help with:

- A first-home deposit

- Third-level education costs

- A first car

- Starting a business

- Other major life expenses

By planning ahead and using annual exemptions consistently, families can provide meaningful financial support for future generations. They can also improve overall tax efficiency.

Practical Considerations

Using the Small Gift Exemption is relatively straightforward. The gift must be made during the relevant calendar year and should be supported by appropriate records, such as bank transfers or payment references.

Families may benefit from coordinating gifts between parents, grandparents, and other relatives to ensure available exemptions are fully utilised each year.

While the Small Gift Exemption is valuable in its own right, it is often most effective when incorporated into a broader financial and estate-planning strategy. Consideration should also be given to wills, pensions, investments, and other available tax planning opportunities to ensure wealth is transferred as efficiently as possible.

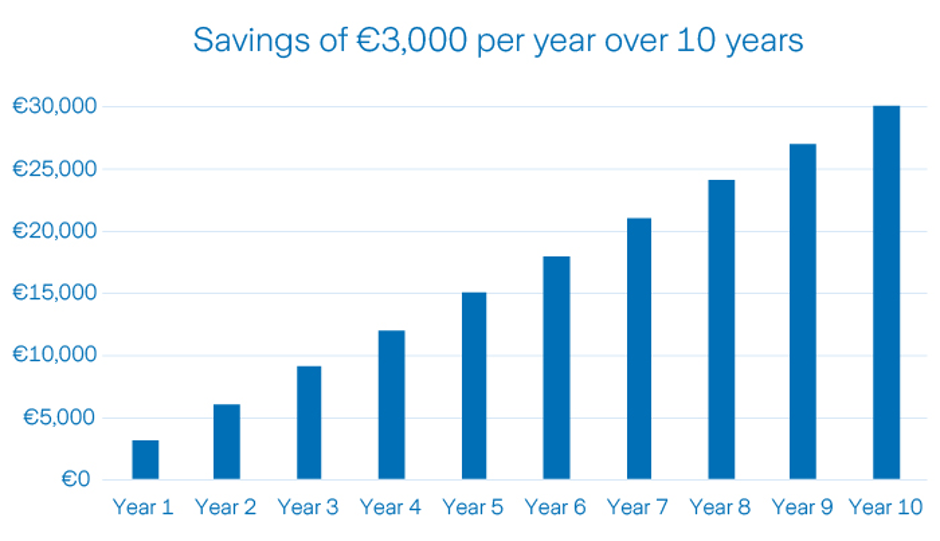

What would happen if I ‘gifted’ €3,000 to my daughter each year?

Assuming a parent gifted €3,000 into an account, which gave no interest nor any fund growth, there would still be a considerable fund available to your daughter. And she’d have no liability to any Capital Acquisitions Tax on that fund. After 10 years, she would have €30,000 available to her for a house deposit, a new car, or to fund that trip around the world.

Reference: Helping family members with money https://www.zurich.ie/blog/helping-family-members-with-money/

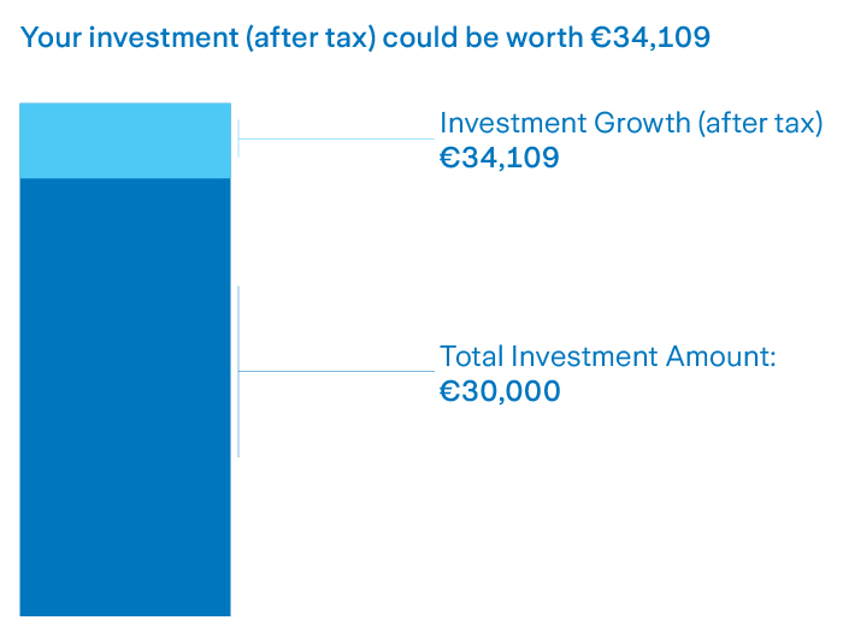

See how your gift can grow over time

By choosing to invest your yearly gift, it’s possible for the total value to surpass the original investment. Assuming an annual growth rate, your gift of €3,000 per year over 10 years could be worth more than the total amount saved. Investing for growth helps you make the most of every contribution.

Utilising the Small Gift Exemption with Zurich

To help people take advantage of the small gift exemption in a streamlined and efficient manner, 20 years ago Zurich created the Child Savings Plan, now also known as the Small Gift Saver.

Minor Children under age 18 at outset

If the person you are saving for is a minor child under 18 years old, Zurich’s Small Gift Saver, a unique plan where the child owns the policy to which the money can be contributed by you, the payor.

This is done by way of an Assignment, a transfer of ownership from the original policy owners to the minor child. Again, once the annual contribution or monthly equivalent is €3,000 per calendar year, no liability to CAT will arise.

Children over age 18 at outset

If the person you are saving for is over 18, they can take out any of Zurich’s selection of savings policies and you, as the payor, can pay the contributions into that policy. If the annual contribution is €3,000 per calendar year, no liability to CAT will arise.

Zurich’s savings policies are ideal for you to gift money to your loved ones, accumulating a fund which they can use for something they might need in the future, a deposit for a house, a holiday, or a new car.

The information contained herein is based on Zurich Life’s understanding of current Revenue practice as at January 2026 and may change in the future.

Reference and Source: Helping family members with money https://www.zurich.ie/blog/helping-family-members-with-money/

Frequently Asked Questions

Can I gift €3,000 to each child every year tax-free?

Yes. Under Ireland’s Small Gift Exemption, an individual can gift up to €3,000 per year to another person without impacting their Capital Acquisitions Tax threshold.

Can both parents gift €3,000 each?

Yes. A couple can gift a combined €6,000 per year to one child.

Does the Small Gift Exemption affect inheritance tax thresholds?

No. Gifts made under the exemption do not reduce the beneficiary’s lifetime CAT threshold.

Can grandparents use the exemption?

Yes. Grandparents can also gift €3,000 annually to each grandchild.

Need help creating a tax-efficient gifting strategy?

If you’d like to explore how a savings plan and the Small Gift Exemption could fit into your overall financial strategy, contact Stephen at Donnelly Financial Planning. We can help you build a personalised savings and estate planning solution designed around your family’s long-term goals.

The Small Gift Exemption is one of the simplest yet most powerful wealth transfer tools available to Irish families. When combined with a structured savings plan, it can help parents and grandparents support future generations while reducing potential inheritance tax liabilities. Starting early can make a significant difference over time.

Sources and References

- Revenue Commissioners, Capital Acquisitions Tax (CAT): Thresholds, Rates and Aggregation Rules.

- Revenue Commissioners, Gift and Inheritance Tax (CAT).

- Zurich Life Assurance plc, Helping Family Members with Money.

https://www.zurich.ie/blog/helping-family-members-with-money

This article is based on Revenue guidance and tax thresholds as understood at the time of publication. Tax rules, thresholds and reliefs may change, and individual circumstances may affect tax treatment. The information provided is for general guidance only, and professional advice should be sought before making any financial or tax-related decisions.

Disclaimer: This article is for general information purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change in the future. You should seek professional advice before making financial decisions.

Donnelly Financial Planning Ltd is regulated by the Central Bank of Ireland.