If you’ve worked hard all your life to build up your home, savings, investments or even a family business, you’ll probably want to pass as much of that wealth as possible to the people you care about.

An inheritance can sometimes bring a tax bill. In Ireland, Capital Acquisitions Tax (CAT) may apply when someone receives a gift or inheritance above certain tax-free thresholds.

Over the years, I’ve spoken with many people who assumed their family would simply inherit everything they owned. They hadn’t considered that their children or other beneficiaries might have to find a substantial amount of money to pay Revenue.

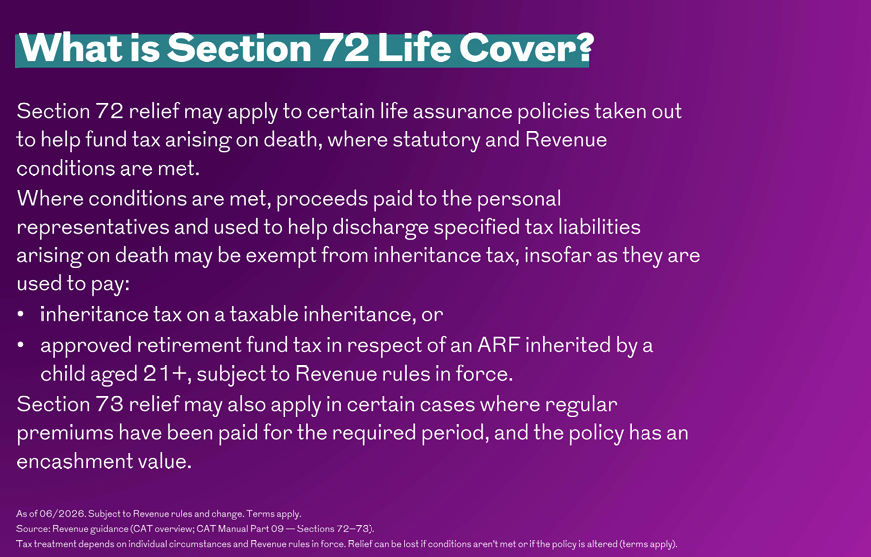

That’s where Section 72 Life Cover can be worth exploring.

Section 72 Life Cover is a special type of Whole of Life insurance that can help provide funds to meet a future inheritance tax liability, helping families protect the assets they have worked hard to build.

Understanding Capital Acquisitions Tax

Capital Acquisitions Tax, or CAT, is a tax that may apply when someone receives an inheritance after a death or a gift during someone’s lifetime.

Whether CAT is payable depends on several factors, including the relationship between the person giving the gift and the person receiving it, the value of the inheritance and whether the beneficiary has already received previous gifts or inheritances within the same tax threshold.

There are some important exemptions. For example, gifts and inheritances between spouses or civil partners are generally exempt from CAT. There is also a Small Gift Exemption that currently allows someone to receive up to €3,000 each year from an individual without affecting their lifetime tax free threshold.

As with all tax legislation, these rules and thresholds can change over time, which is why it is always important to seek professional financial and tax advice.

So, What is Section 72?

Section 72 Life Cover refers to a specific type of Whole of Life assurance policy that is designed to help pay an inheritance tax liability.

How It Can Help

Provided certain Revenue conditions are met, the proceeds from the policy may be used to help pay qualifying inheritance tax arising on death.

Why It Matters

In simple terms, it is about creating a fund that can provide cash when your family needs it most. Instead of having to sell property or other valuable assets to pay a tax bill, there may already be money available to meet that liability. For many families, that can provide real peace of mind.

The diagram above gives a simple overview of how a Section 72 Life Cover policy can help provide funds to meet a potential inheritance tax liability, subject to Revenue rules.

Why is This Important?

Today, many people have built up considerable wealth without necessarily thinking of themselves as wealthy.

A family home that was bought many years ago may now be worth significantly more than expected. The same can be true of investment properties, farmland or a family business. While these assets may be valuable, they do not always provide immediate access to cash.

If an inheritance tax bill arises, beneficiaries may need to borrow money or even sell assets that were intended to stay within the family. Planning can help avoid that situation.

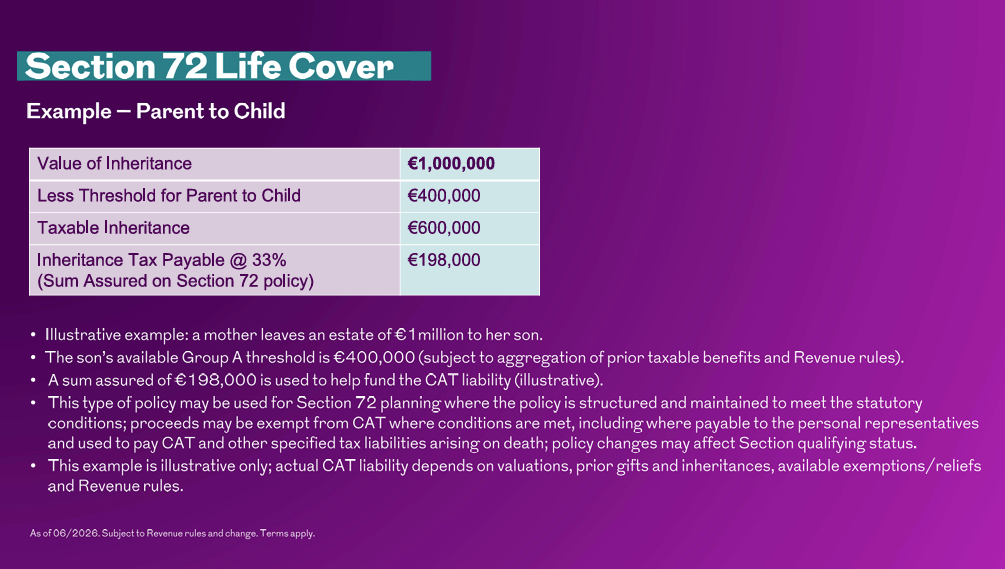

An Example

The example below illustrates how an inheritance tax liability can arise when an estate exceeds the available tax free threshold.

Let’s imagine a mother leaves an estate valued at €1 million to her son.

If the available Group A threshold is €400,000, the remaining €600,000 could potentially be liable to Capital Acquisitions Tax. At the current CAT rate of 33%, that could result in a tax bill of almost €200,000.

Finding that amount of money at short notice is not easy for most families. A Section 72 Life Cover policy, if arranged correctly and subject to Revenue rules, can provide funds that may be used to help pay that liability, allowing the family to retain the assets they have inherited.

Please note that this example is for illustration purposes only. Tax thresholds and rates may change, and your own circumstances will determine any potential tax liability.

Is Section 72 Right for Everyone?

Not necessarily.

Every family is different and every estate is different.

Whether Section 72 is appropriate depends on the value of your estate, your family circumstances, your health and the potential tax liability your beneficiaries may face in the future.

That is why it is important not to make assumptions or rely on general information alone.

A Final Thought

One thing I’ve found over the years is that many people assume their family will simply inherit everything they own. Often, they don’t realise that there may also be an inheritance tax bill to consider.

It is about giving your family choices and making life a little easier for them when they need it most.

Putting a plan in place today can help protect the wealth you have worked so hard to build and provide peace of mind for the people you love.

If you are unsure whether your estate could be affected by Capital Acquisitions Tax, I would encourage you to have a conversation with a qualified financial adviser. Together, you can review your circumstances, estimate any potential tax liability and decide whether Section 72 Life Cover could form part of your overall financial plan.

Every situation is unique, and the right advice is always based on your own personal circumstances. Sometimes, the best financial decisions begin with simply understanding your options.

Thinking About Your Own Situation?

Understanding inheritance tax and the options available to you can feel overwhelming. Every family is different, and what works for one person may not be the right solution for another.

That is why I always recommend having a conversation before making any decisions.

If you are wondering whether your estate could be affected by Capital Acquisitions Tax, or you would simply like to understand how Section 72 Life Cover works, I would be happy to talk you through it in plain English.

Together, we can look at your circumstances, discuss your options and help you understand what may be appropriate for you and your family. There is absolutely no obligation, just clear, professional advice to help you make informed decisions.

Book an Appointment with Stephen Donnelly

If you would like to arrange a confidential, no obligation chat about Section 72 Life Cover or any aspect of inheritance tax planning, I’d be delighted to discuss your options.

📅 Book an Appointment: Stephen Donnelly Director

📧 Email: stephen@dfp.ie

🌐 Website: https://www.dfp.ie

Stephen Donnelly, QFA is a Qualified Financial Adviser with Donnelly Financial Planning. He helps individuals, families and business owners in Ireland make informed financial decisions, from protecting their loved ones to planning for retirement and passing wealth to the next generation.

References

Graphic Source

Royal London Ireland Adviser Technical Marketing Material. Graphics reproduced with permission for educational purposes.

Article Reference:

Stephen Donnelly, QFA, prepared this article using educational material from Royal London Ireland, together with general guidance on Capital Acquisitions Tax (CAT) and Section 72 relief under current Irish Revenue legislation. The information is provided for general guidance only and does not constitute financial, tax or legal advice.

Sources

Capital Acquisitions Tax Consolidation Act 2003, Section 72

Revenue.ie, CAT thresholds and rates

Revenue.ie, CAT groups

Disclaimer

Important Information: This article is provided for general information purposes only and does not constitute financial, tax or legal advice. It should not be relied upon as a substitute for professional advice tailored to your individual circumstances.

Tax treatment depends on the personal circumstances of each client and may change in the future. Before making any financial planning decisions, you should seek advice from a qualified financial adviser and, where appropriate, an independent tax or legal adviser.

The views expressed in this article are those of the author at the date of publication and may change without notice. While every effort has been made to ensure the information is accurate and up to date, no guarantee is given regarding its completeness or accuracy, and no responsibility is accepted for any loss arising from reliance on its contents.

Life insurance policies are subject to underwriting, acceptance by the insurer and the completion of a full application. Additional medical or health information may be required, which could affect eligibility for cover or the premium payable.

Donnelly Financial Planning Ltd is regulated by the Central Bank of Ireland